Business

5 Ways to Make a Remarkable Recovery From Bankruptcy

No one dreams about or looks forward to the day where they have to file for bankruptcy. However, life is filled with unpredictable events which may harm your financial stability and consequently cause bankruptcy.

Although going through this stressful and demanding process may seem like you’ve hit rock-bottom, don’t forget that it’s more than possible to recover even from the worst case of bankruptcy. While bouncing back from it will require some time and additional management until your credit is sorted, you’ll have a fresh start with your finances once you complete it.

So, if you’re ready to transform your current financial state and ensure it flourishes in several years, make sure to follow the steps mentioned in this article.

Make a Detailed Financial Plan

Bankruptcy makes drastic changes to your financial plans, assets, payments, and much more. For that reason, the best thing to do is make a completely new financial plan that will be more appropriate with your current budget. You’ll need to include your business, property, income, fixed payments, and several other things to make a realistic financial plan for the fastest recovery.

Starting a post-bankruptcy plan might seem overwhelming since you’ll need to go back to the roots of business planning and budget management, so hiring a local bankruptcy attorney can be a great deal of help to you.

Also, bankruptcy paperwork contains pages and pages of unfamiliar concepts and phrases, so dealing with it on your own can be pretty challenging. An attorney specializing in bankruptcy will carefully examine your situation, and together you can create a detailed plan which you won’t have trouble following.

Carefully Follow Your Credit Scores

Your credit scores will change as your bankruptcy process starts evolving. Once you file for bankruptcy, you’ll immediately notice some changes related to your credit scores. However, that doesn’t mean your credits are balanced out. Namely, depending on your bankruptcy type, the credit scores can change even up to several months.

For example, filing for Chapter 7 bankruptcy will initially take a more significant amount, but you’ll also notice minor dips once your case is discharged. On the other hand, Chapter 13 bankruptcy isn’t discharged until the end of the repayment period.

Some people even witness small credit score increases after filing for Chapter 13 because their score fell as far as it can go before filing for bankruptcy.

So, to take advantage of your credit scores in the best possible way, the best thing to do is track your status several months after filing or after your case has been discharged.

Respect Deadlines

Keeping track of your payment deadlines is always essential, but it’s even more emphasized if you went through bankruptcy. After that rough patch, you’ll most likely have difficulties finding lenders, vendors, or banks willing to lend you money and help you stay on your feet. However, even when you do find them, they’ll keep a close eye on each payment.

Missing deadlines and being late with your payments won’t set a good example for you and your business, so it’s unlikely anyone will prolong to offer their services to you. Instead, make sure to pay on time. Not only will this show you’re serious about your business, but also that you respect your lenders.

Make Smart Financial Decisions

It’s essential to look at bankruptcy from a positive side too. This process enables you to erase all your previous debts and start from scratch. Although you may think this is the end of your business ventures, you’ll quickly realize bankruptcy is a chance for you to rebuild your entire life and make smarter financial decisions than in the past.

Some people feel overconfident after going through bankruptcy because their debts are paid off. Hence, they take advantage of their financial situation and get more credits to cover their current expenses. However, as the credit limit rises over time, it’s harder to maintain the balance.

When you go through bankruptcy, you should pay close attention to every decision regarding money to ensure you’re doing everything in your power to get back on track.

Learn From Previous Mistakes

Bankruptcy will teach you a valuable lesson about finances and their management. The best way to avoid the repetition of the same mistake is to go back and see what caused the bankruptcy in the first place.

Work hard on resolving the issue, no matter what it was. If you don’t get to the core of the problem, you’ll just make the same mistake, leading you to the same ending.

The presence of an optimistic attitude and willingness to change is the main reason why some people flourish after bankruptcy, so make sure you learn from your past mistakes.

Conclusion

All in all, going through bankruptcy demotivates many people. However, how you deal with it and what you do to correct your mistakes is a crucial step. By following these five ways, you’ll make a remarkable recovery from bankruptcy. These steps will allow you to carefully assess your previous mistakes and current affairs for a brighter and more prosperous future.

Clinical Trials Market Set for Robust Growth, Driven by Drug Development Surge and Digital Innovation

Pediatric Vaccines Market: Safeguarding Futures, Driving Growth

Faropenem Sodium Market: A Potent Weapon in the Fight Against Bacterial Infections

Downhole Tools Market: Navigating Subsurface Frontiers with Precision

Waterproof Structural Adhesives Market: A Comprehensive Study Towards USD 10.3 Billion in 2035

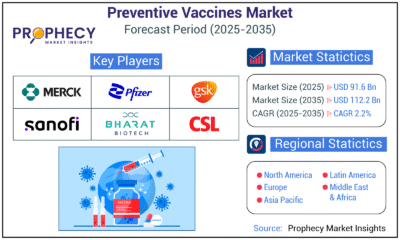

Preventive Vaccines Market to Witness Strong Growth by 2035

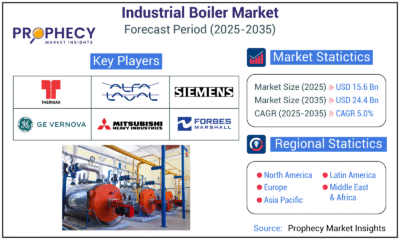

Industrial Boiler Market Expected to Surpass USD 24.4 Billion by 2035 Amid Growing Demand for Energy Efficiency and Industrialization

Fill-Finish Pharmaceutical Contract Manufacturing Market Expected to Flourish Amid Biopharmaceutical Boom and Global Outsourcing Trend by 2035

Pet Food Nutraceutical Market Set for Robust Expansion Amid Rising Demand for Pet Wellness by 2035

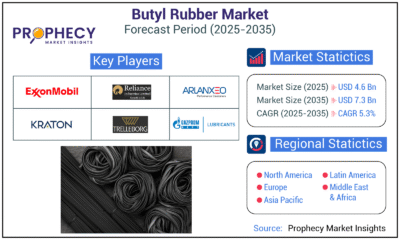

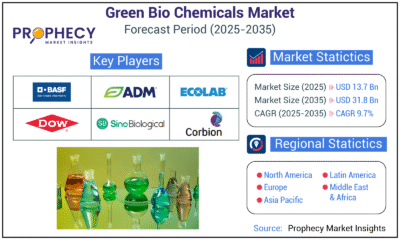

Green Bio Chemicals Market Poised for Sustainable Growth amidst Global Shift to Eco-Friendly Alternatives by 2035

Cat Food Market Forecast 2035: Natural Ingredients, Pet Wellness to Lead the Way

How Managed IT Solutions Help Small Teams Compete at Enterprise Scale

Why Alaxio (ALX) Is a Top Pick for Smart Crypto Investors

Bellarium ($BEL) Price Prediction: Could It Hit $5 by 2026?

Crypto WINNAZ Launches First On-Chain Yield Engine for Meme Coins, Enabling 20x–300x Returns

-

Press Release4 days ago

Press Release4 days agoClinical Trials Market Set for Robust Growth, Driven by Drug Development Surge and Digital Innovation

-

Press Release5 days ago

Press Release5 days agoFill-Finish Pharmaceutical Contract Manufacturing Market Expected to Flourish Amid Biopharmaceutical Boom and Global Outsourcing Trend by 2035

-

Business6 days ago

Business6 days agoHow Managed IT Solutions Help Small Teams Compete at Enterprise Scale

-

Press Release5 days ago

Press Release5 days agoGreen Bio Chemicals Market Poised for Sustainable Growth amidst Global Shift to Eco-Friendly Alternatives by 2035

-

Press Release5 days ago

Press Release5 days agoIndustrial Boiler Market Expected to Surpass USD 24.4 Billion by 2035 Amid Growing Demand for Energy Efficiency and Industrialization

-

Press Release5 days ago

Press Release5 days agoPreventive Vaccines Market to Witness Strong Growth by 2035

-

Press Release5 days ago

Press Release5 days agoPet Food Nutraceutical Market Set for Robust Expansion Amid Rising Demand for Pet Wellness by 2035

-

Press Release5 days ago

Press Release5 days agoWaterproof Structural Adhesives Market: A Comprehensive Study Towards USD 10.3 Billion in 2035